ALL BLOG CONTENT IS FOR INFORMATIONAL PURPOSES ONLY. ANY REFERENCE TO OR MENTION OF INDIVIDUAL STOCKS, INDEXES, OR OTHER SECURITIES ARE NOT RECOMMENDATIONS AND ARE SPECIFICALLY NOT REFERENCED AS PAST RECOMMENDATIONS OF PATTON WEALTH ADVISORS. ALL GRAPHS, CHARTS, AND TABLES ARE PROVIDED FOR ILLUSTRATION PURPOSES ONLY. EXPRESSIONS OF OPINION ARE ALSO NOT RECOMMENDATIONS AND ARE SUBJECT TO CHANGE WITHOUT NOTICE IN REACTION TO SHIFTING MARKET, ECONOMIC, OR POLITICAL CONDITIONS. IT IS COMMON FOR US TO USE A FUND AS A PROXY FOR AN INDEX OR ASSET CLASS. FOR MORE DETAILS SEE OUR FULL DISCLOSURE HERE.

Market Commentary - Week Ending 3/17/2018

Summary

Inflation fears recede with multiple economic reports showing moderation

Retail sales disappoint for a third consecutive month helping bond prices

Technology stocks continue to lead the market in 2018

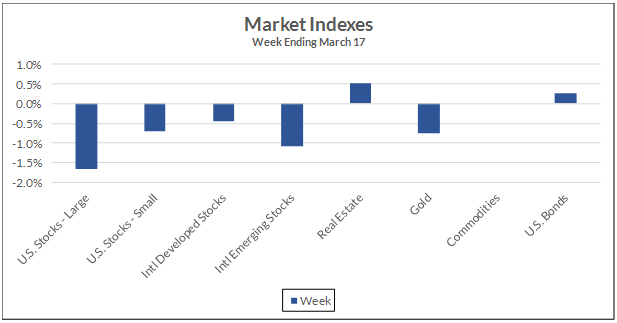

Stocks around the world declined for the week with large U.S. stocks leading the way. Every day of the week was marked by some optimism in the morning that was followed by declining prices throughout the day and ending every day lower than they opened. For the week large U.S. stocks were off -1.7% while small U.S. stocks held up much better declining just -0.7%. Year-to-date small stocks hold a lead over large stocks with gains of +3.5% for small stocks and +2.8% for large.

The largest technology stocks continue to be the best performers in 2018 in spite of some fear that these stocks had overheated in 2017 and early 2018. Year-to-date technology stocks are higher by +10.7% and only slipped -1.0% for the week. The real outlier for the week though were utility stocks rallying +2.5%, following bonds higher on a weak economic report on Wednesday, and continued higher the remainder of the week. In spite of the week’s big gain, utilities remain lower for the year by -4.0%.

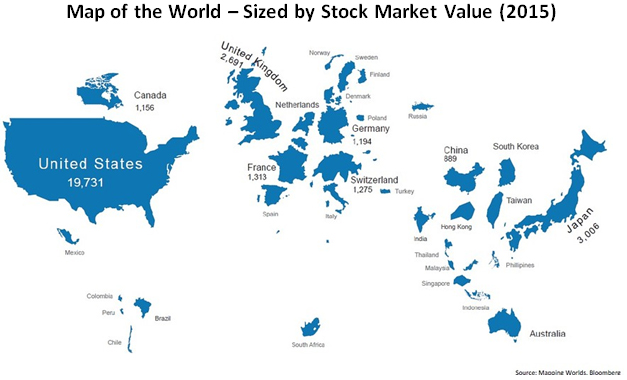

International stocks decline along with U.S. stocks but did hold up relatively well. For the week, international developed stocks loss just -0.4% and are now just fractionally higher year-to-date. European markets held up fairly well while Australia’s market declined -2.3%. International emerging markets were lower by -1.1% but still hold the lead for 2018 with a gain of +4.4%. Brazil’s market, one of the best performing in 2018 with a gain of +10.3%, lost -3.0% this week. Another surprising year-to-date winner is Russia’s market up +9.0% but lower this week by -2.8%. It needs to be noted that Russia’s market is very small compared to others in the world as illustrated in the accompany graphic that sizes each country by the market value of its stock market.

Along with international stocks, non-traditional investments also held up better this week than U.S. stocks. Real estate did the best, up +0.5% for the week, as nearly all interest rate sensitive investments gained ground. This small gain helped ease the pain for investors in real estate but this group remains down -7.7% for 2018. Commodities were flat for the week and are up fractionally year-to-date. Gold declined by -0.7% as fears of inflation subsided.

Bonds posted one of their better week’s performances for 2018 with a gain of +0.3%. Helping prices this week were multiple economic reports including one showing weak retail sales and two others indicated inflation is less of a concern than thought just 30 days ago. Year-to-date the bond market remains lower by -2.5%.

Stock Highlights

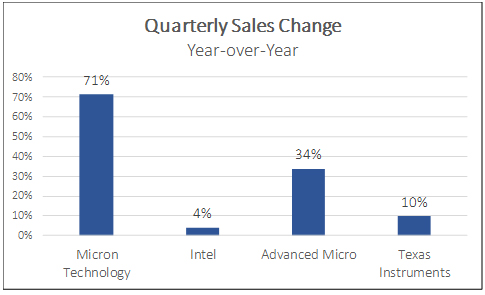

Micron Technology (MU), a computer chip maker, received positive comments from Wall Street analysts that pushed its stock higher for the week by +11.0%. These analysts are optimistic about the company’s outlook helped by recent sales gains as illustrated in the accompanying graph. This stock has had a great start to 2018 with a gain of +47.3% following a 2017 gain of +87.6%!

Dollar General (DG), a $23 billion in sales discount retailer, reported better than expected quarterly results including same-store sales higher by a very impressive +7.5%. The company went on to raise earnings estimates for 2018, increased its dividend by +12%, and authorized an increase in its share repurchase program by $1 billion. These strong results were well received by investors with the stock higher for the week by +9.8% which brought it into positive territory for the year by +2.6%.

Activision Blizzard (ATVI), a maker of video games with a $54 billion market value, saw its stock decline by -8.4% during the week. The stock has had a strong start in 2018 still higher by +13.2% in spite of this week’s loss. This company has some extremely successful game franchises including Candy Crush and Call of Duty. The business has though gone through a long period of nearly no sales growth from 2010 – 2016 that could cause some concerns about the future for investors.

Boeing (BA), a world leading aircraft manufacturer, has seen its stock drift lower the past three week on fears that tariffs will be a negative for the company. The stock fell -6.8% for the week, losing -14.1 billion in market value, and is now off nearly -10% from its peak a few weeks ago. In spite of this loss, the stock is still higher by +12.1% but the recent trend, combined with headlines about possible trade wars, could have shareholders concerned.

Economic Indicator - Reported

February Retail Sales were clearly a disappointment showing a decline of -0.1% for the month as compared to economists’ average estimate of a gain of +0.4%. This now is the third consecutive month of declines raising some concerns about overall economic growth in the first quarter and beyond. There was a lot of optimism for February that numbers would be strong as consumers begin to see the benefits of the big tax cuts.

Easing some concerns about consumer spending is that the overall retail sales report was meaningfully impacted by a not-surprising -0.9% drop in vehicle sales due to hurricanes in 2017 that pulled sales forward. Furthermore, the year-over-year overall numbers remain strong at +4.0%.

Inflation fears meaningfully eased with the February Consumer Price Index (CPI) showing an as expected gain of +0.2%. This comes off the January report that helped rock the stock market showing prices higher by +0.5%. Helping hold down prices were vehicles prices lower by -0.5%, as discounting persists due to weak sales, and communications costs (wireless phone costs) down -0.5%.The Producer Price Index (PPI) also came in at +0.2% as economists had expected. This follows a January report of +0.4%.

Economic Indicators – Upcoming

Two reports will provide an update on the housing markets. Existing home sales are expected to be lower by -3.2% for the month and -4.8% compared to the same time last year. There continues to be a lack of homes for sale creating the slow sales environment.

One of the reasons for fewer existing homes for sale is that new home construction is near a 60-year record low according to Federal Reserve Bank data. This is being impacted by both higher land and construction costs. A report on New Homes Sales for February is expected this week.

Durable Goods Orders, new orders placed with domestic factories, are expected to increase by +1.7% in February according to economists’ estimates. This would be a strong rebound from January’s -3.7% that was significantly impacted by a drop in aircraft-related orders. The core number, excluding transportation, is expected to be strong at +0.6% as compared to January’s -0.2%.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. Any specific securities or investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own situation before making any investment decision including whether to retain an investment adviser.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. This content was created as of the specific date indicated and reflects the author’s views as of that date. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results. Any comments about the performance of securities, markets, or indexes and any opinions presented are not to be viewed as indicators of future performance.

Investing involves risk including loss of principal.

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. For more information on specific indexes please see full disclosure here.

Any charts, tables, forecasts, etc. contained herein are for illustrative purposes only, may be based upon proprietary research, and are developed through analysis of historical public data.

All corporate names shown above are for illustrative purposes only and are NOT recommendations.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

IMPORTANT NOTICE: INFORMATION ABOUT PAST PERFORMANCE

Not indicative of future returns. Past performance is not indicative of future returns, which may vary. Accordingly, future returns are not guaranteed and there can be no assurance that any Patton Fund, Strategy, or Portfolio (“Patton Investments”) will achieve comparable investment results or its investment objective. You may lose money on your investment in a Patton Investment.

Strategy Developed based on Back-testing. The investment strategies used by Patton were developed, in part, by back-testing its investment program against past market and economic conditions. In other words, the strategies were designed to succeed based on knowledge of events that occurred in the past. One limitation of such a strategy is that it is inherently focused on the past, and cannot necessarily take account of market and economic conditions that may arise in the future. If future market and economic conditions are different from past market and economic conditions, and if investors behave differently from past investors, Patton’s investment strategies may not work as anticipated and the Strategy, Fund, or any Patton Investments, may lose money.

Fees and Distributions. The performance information shown reflects the deduction of actual expenses of the applicable Patton Investment for periods during which the Patton Investment has been in operation (see below). The performance figures shown reflect the reinvestment of all dividends, interest and other income, and assume that the applicable Patton Investment has not made any distributions to investors. Estimated fees and expenses including brokerage commissions, borrowing costs, and advisory fees, have been deducted from all back-tested performance.

Portfolio Characteristics. Portfolio characteristics, including specific holdings, contributors to performance, and country, sector and industry exposure, are shown as of the date indicated only, and are subject to change without notice. Portfolio characteristics are designed to illustrate the application of the Patton Investments’ investment style only, and should not be considered a recommendation.

Third Party Information. Information contained herein is based on data obtained from statistical services, company reports or communications, or other sources. Patton Fund Management believes these sources to be reliable. However, we have not verified this information, and we make no representations whatsoever as to its accuracy or completeness.

IMPORTANT NOTICE: INFORMATION ABOUT BACK-TESTED PAST PERFORMANCE

Performance results may be presented that pre-dates the commencement of operations of a Patton Investment Strategy. Because the Patton Investment Strategy was not in operation during certain periods shown, the performance information prior to the date the Patton Investment Strategy commenced operations is back-tested performance (sometimes referred to as hypothetical performance).

Patton Investment Strategies Inception Dates (first full month)

Patton 45: April 2001 (not open to new investors)

Patton Edge Strategy: February 2010

Patton Flex Strategy: February 2010

Audacity Strategy: April 2020

There are several important factors to consider when reviewing back-tested, or hypothetical, performance information:

Back-tested Performance is Hypothetical. The performance information shown for the Patton Investment Strategy you select includes performance information that is hypothetical, and is not real nor based on an actual portfolio managed by Patton. As such, the back-tested portion of the performance presentation does not represent the investment performance or the actual Patton Investment Strategy or any investors in the Patton Investment Strategy. The securities in these hypothetical portfolios were selected with the full benefit of hindsight, after their performance over the period shown was known. It is not likely that similar results could be achieved in the future. The back-tested results may not reflect the impact that any material market or economic factors might have had on the results if the Strategy had been used during the period to actually manage client assets. Furthermore, back-testing does not reflect how Patton actually might have reacted when managing client investments to economic and market events.The hypothetical portfolios presented here are purely illustrative, and representative only of a small sample of possible future scenarios.

Back-testing is Subject to Limitations. While it is believed that back-tested performance information presented is relevant to evaluating an investment in the Patton Investment Strategy, no representation is or could be made that the information presents what the performance results would have been in the past or are likely to be in the future. There are frequently sharp differences between hypothetical performance results and actual performance results subsequently achieved. One limitation of hypothetical performance is that it is generally prepared with the benefit of hindsight. In addition, no hypothetical track record can completely account for the impact of financial risk in actual trading. For example, back-factors that affect markets in general, the impact of fees and expenses, market liquidity and other factors may all have affected actual performance.

Actual Investor Experience Varies. The back-tested results are not indicative of the skill of Patton. For example, each Patton Investment Strategy began trading on the date indicated above. Back-tested performance shown for each Patton Investment Strategy reflects hypothetical performance determined using the current investment strategy of the applicable Patton Investment Strategy. However, Patton has been managing money using quantitative strategies since 2001. During this period Patton has experienced periods of poor performance and Patton has closed other Patton Investment Strategies that it has managed as a result of poor performance. Investors in some of Patton’s closed Strategies (and funds) have lost money.

Back-testing Period. During the back-tested period, Patton was either not providing investment advice or was not providing investment advice according to the Strategy used to calculate the back-tested results.

Indices. The historical performance of various indices, such as the S&P 500 Index, may be included. An index is an unmanaged, broad-based market index and investing in any Patton Investment Strategy is not similar to investing in an index. An index is not available for direct investment, and the securities in an index will not match the Strategy's holdings. In addition, unlike an index, the Strategy's performance will be affected by fees and expenses.

Forward-looking Statements. Any forward-looking statements represent the subjective views of Patton and their validity may be affected by events and conditions not now contemplated and by other factors, many of which may be beyond Patton's control. Actual results may vary and such variations may be material, and no representation or warranty is made regarding any forward-looking information contained herein.

Patton Strategy Composites

Patton Edge Strategy Actual Results.Performance results for February 2010 forward represents a dollar-weighted average of all accounts utilizing this strategy. The net return is the gross return reduced by 1/12 of 2.0% monthly. NOTE - an enhancement was made to the Strategy in March 2021 that is expected to have a meaningful impact on the performance of the Strategy in the future during the early months of a bull market.

Patton Edge Performance Statistics:

Start

End

Composite Return

Portfolio Count

Portfolio Count (End Period)

End Capital

12/31/2010

12/31/2011

9.53

3

8

1,692,849

12/31/2011

12/31/2012

11.26

5

8

1,683,360

12/31/2012

12/31/2013

27.11

6

11

2,236,018

12/31/2013

12/31/2014

11.93

8

14

1,188,751

12/31/2014

05/31/2015

0.00

14

17

1,697,507

12/31/2014

12/31/2015

5.29

13

19

1,656,694

12/31/2015

12/31/2016

-5.88

15

28

2,558,860

12/31/2016

12/31/2017

18.60

23

31

2,675,077

12/31/2017

12/31/2018

-4.54

14

18

994,749

12/31/2018

12/31/2019

15.06

14

14

841,753

12/31/2019

12/31/2020

-0.41

12

12

573,401

12/31/2020

12/31/2021

10.79

10

10

597,863

12/31/2021

12/31/2022

1.94

8

8

441,354

12/31/2022

12/31/2023

4.22

6

6

360,066

12/31/2023

12/31/2024

21.35

6

6

385,304

12/31/2024

01/31/2025

0.00

6

6

403,712

Patton Flex Strategy Actual Results.Performance results for February 2010 forward represents a dollar-weighted average of all accounts utilizing this strategy. The net return is the gross return reduced by 1/12 of 1.5% monthly. A performance-based fee structure is charged to some investors utilizing the Patton Flex Strategy that could result in higher fees than 1/12 of 1.5% annually. NOTE - an enhancement was made to the Strategy in March 2021 that is expected to have a meaningful impact on the performance of the Strategy in the future during the early months of a bull market.

Patton Flex Performance Statistics:

Start

End

Composite Return

Portfolio Count

Portfolio Count (End Period)

End Capital

01/31/2010

12/31/2010

13.85

1

1

1,142,400

12/31/2010

12/31/2011

22.48

1

1

1,739,954

12/31/2011

12/31/2012

34.24

1

1

3,114,146

12/31/2012

12/31/2013

68.92

1

1

5,074,023

12/31/2013

12/31/2014

22.43

1

1

11,795,197

12/31/2014

12/31/2015

25.79

1

1

24,493,849

12/31/2015

12/31/2016

-7.66

1

6

31,760,856

12/31/2016

12/31/2017

40.16

4

16

54,716,935

12/31/2017

12/31/2018

-13.95

15

42

61,359,349

12/31/2018

12/31/2019

17.73

29

45

79,211,768

12/31/2019

12/31/2020

-2.69

36

47

74,874,709

12/31/2020

12/31/2021

29.15

34

47

92,471,626

12/31/2021

12/31/2022

-2.55

41

49

88,897,349

07/31/2022

12/31/2022

-5.97

45

50

88,900,320

12/31/2022

12/31/2023

2.62

42

52

91,036,035

12/31/2023

12/31/2024

42.29

48

50

117,371,667

12/31/2024

01/31/2025

0.00

50

50

133,515,832

Audacity Performance Actual Results. Performance results for April 2020 forward represents a dollar-weighted average of all accounts utilizing this strategy. The net return is the gross return reduced by 1/12 of 4.0% monthly. A performance-based fee structure is charged to some investors utilizing the Audacity Strategy that could result in higher fees than the monthly management fee deducted from this data. NOTE - an enhancement was made to the Strategy in March 2021 that is expected to have a meaningful impact on the performance of the Strategy in the future during the early months of a bull market.

Audacity Performance Statistics:

Start

End

Composite Return

Portfolio Count

Portfolio Count (End Period)

End Capital

03/31/2020

12/31/2020

8.96

2

2

7,437,680

12/31/2020

12/31/2021

49.97

2

2

9,652,268

12/31/2021

12/31/2022

-7.29

2

2

11,523,894

12/31/2022

12/31/2023

-3.24

2

2

11,373,001

12/31/2023

12/31/2024

45.38

2

2

13,970,462

12/31/2024

01/31/2025

0.00

2

2

16,913,896

Notes about Composites:

"n/a" - Not statistically meaningful due to insufficient number of months.

Dispersion: Performance dispersion is calculated annually. Portfolios are only included that were in the strategy for the full year. Dispersion is calculated by subtracting the lowest portfolio return from the highest portfolio return.

Benchmark Description: The benchmark is the HFRX Equity Hedge index obtained from www.HedgeFundResearch.com. This is an investable index of long/short U.S. equity hedge funds. Its composition of securities and risk profile could be meaningfully different than the Patton Investment Strategy.

The above composite performance presentation for the Patton Edge Strategy and the underlying methodology used was independently verified by Ashland Partners only for the period through 12/31/2014. The above composite performance presentation for both the Patton Flex Strategy and Audacity Strategy and the underlying methodology used are identical to that of the Patton Edge Strategy.

Leverage: the Patton Edge Strategy can have up to two times gross exposure; the Patton Flex Strategy can have up to five times gross exposure; the Audacity Strategy can have up to eight times gross exposure.

The Patton Flex Fund, L.P., utilizing the Patton Flex Strategy, has a 0% management fee, 12% net annual hurdle, and a 50% incentive fee above the annual hurdle. See the Fund's Private Placement Memorandum for details. This fee structure can result in a meaningfully different net performance for investors.

The Audacity Fund, L.P., utilizing the Audacity Strategy, has a 2.0% management fee, 0% net annual hurdle, and a 20% incentive fee above the annual hurdle. See the Fund's Private Placement Memorandum for details. This fee structure can result in a meaningfully different net performance for investors.

Audacity Strategy Back-tested Performance: all performance is shown net of a 4.0% annual management fee. The Strategy is also offered with a 2.0% annual management fee and a 20% annual performance fee on all gains above 0%. Based upon research the 4.0% management fee structure is expected to be the lesser costly of the two fee structures.

Accounts are generally added to a Composite for the first full month invested and removed after the last full month invested.

The Strategy is sometimes carved out of accounts that contain other assets.

Super-Diversification Flex Growth Strategy

This is the actual NET performance of our clients utilizing our Super-Diversification Flex Growth Strategy totaling approximately $116,487,797 of assets. Our Strategy and process has remained consistent over the entire period. Not all Patton Clients with the same strategy experienced the same performance due primarly to minor differences in allocations and differences in fees. A very limited number of Patton Clients pay fees from money outside of their portfolio resulting in a higher return. Some clients are Qualified Clients and Accredited Investors as defined by the SEC and may pay a performance-based fee which can meaningfully impact performance.

Use of leverage on a portion of the portfolios represented by this composite return has had a material impact on the performance figures displayed.

Performance includes the reinvestment of dividends and other earnings. Investors may lose money, and are expected to lose money, during significant market declines and other market conditions, in this strategy.

The asset allocation of the strategy has been different than the ARC Private Client Index, resulting in differing performance, although the risk profiles of both have been generally similar. During the period being reported the market has been in an upward trend that has been stronger than historic averages. There is no assurance that this type of trend will persist or how we would perform if it did.

All other representations of Super-Diversification performance throughout our website is back-tested simulated results unless otherwise noted.

ARC Private Client Index

The ARC Private Client Index is an index created by and maintained by the ARC Group. These indexes consist of more than 350,000+ actual investor portfolio returns that are managed by 147 investment managers (as of April 2025) including some of the largest in the world. These 147 managers only represent a sample of the 10,000's of investment managers and other such service providers (financial planners, traditional brokers, etc.).

There are 4 Private Client Indexes each with a different risk profile. We have selected the ARC Private Client Index with the most comparable risk profile, Steady Growth (allocation approximately 46.83% equities, 24.27% Fixed Income, 10.28% Cash, and 18.62% Other as of April 2025), to our Patton Clients performance.

For more information about these indexes, visit the ARC Group's website here.

Industry benchmarks presented for comparison to Super-Diversified Portfolios are believed to be comparable risk portfolios although the holdings are very likely significantly different. Simulated portfolio benchmarks, such as a "Traditional Portfolio", does have a similar risk profile but is allocated only to traditional asset classes of stocks, bonds, and cash.

IMPORTANT NOTICE: INFORMATION ABOUT MODEL PORTFOLIO PERFORMANCE

Unless otherwise noted, the performance of all portfolios ("Model Portfolios") are simulations of various combinations of asset classes used to simulate the performance of various types of portfolios with various risk profiles. All Model Portfolios for all time periods are back-tested hypothetical simulated results.

Model Portfolios have been developed based on historical performance of the described indexes for the relevant time period using our proprietary process and do not represent the results of actual trading of investor assets. Model performance has inherent limitations. Since these are simulated portfolios (hypothetical) and do not reflect any investor's actual experience with owning, trading or managing an actual investment account, there can be no assurance that an investor would have achieved similar rates of return over the time frame. Thus, the performance shown does not reflect the impact that material economic and market factors had or might have had on decision making if actual investor money had been managed. In addition, since the time period in question is a historical one, there can be no assurance that future results achieved by investors will in any way resemble those represented by the Model Portfolios. Model Portfolios are rebalanced monthly. All performance data is total returns which includes interest and dividends. The calculations are net of the estimated management and/or performance fees, trading costs, and fund expense ratios (see below table for estimated expense ratios by Asset Class) if applicable. Performance does not reflect the deduction of other fees or expenses, including but not limited to brokerage account fees, custodial fees, and fees and expenses charged by mutual funds, exchange traded funds, and other investment companies that may be in addition to the expense ratio (these additional expenses tend to be extremely low).

The following describes how a model portfolio monthly return is calculated:

Portfolio Allocation: 50% U.S. Large-Cap, 50% U.S. Aggregate Bonds

Portfolio Fees: 1.2% annually or 0.1% per month

Month's Performance: U.S. Large-Cap = +3.0%, U.S. Aggregate Bonds = +1.0%

Portfolio Performance: (50% x 3.0%) + (50% x 1.0%) = +2.0% less 0.1% (fees) = +1.9%

Model Portfolios presented on our website are portfolios blended from various indexes. The blended asset allocation of every Model Portfolio is readily available within the website. The benchmark index(es) used to represent each asset class is disclosed elsewhere in this disclosure. We do adjust the performance of the benchmark indexes for fees of an applicable fund available to invest in that index or asset class.

When a Model Portfolio's performance is compared to a single benchmark index, such as the S&P 500, the index has not been selected to represent an appropriate benchmark to compare an investor's performance, but rather are disclosed to allow for comparison of the investor's performance, for the convenience of the investor, to that of certain well-known and widely recognized indices. Indices are typically not available for direct investment, are unmanaged, and do not incur fees or expenses.

The goal of a portfolio is not to outperform and single index. The objective of a portfolio is total return. All portfolios are subject to the risk of loss. Patton was not necessarily managing portfolios similar to any given model portfolio. Model Portfolios are not indicative of the skill of Patton nor the performance of portfolios managed by Patton.

The performance calculations of all Model Portfolios have not been audited by any third party. Actual performance of client portfolios may differ materially due to the timing related to additional client deposits or withdrawals and the actual deployment and investment of a client portfolio, the length of time various positions are held, the client’s objectives and restrictions, and fees and expenses incurred by any specific individual portfolio.

Any presentation of two portfolios for comparison is intended to have a similar risk profile. Some Model Portfolios are more diversified than others such as Patton's Super-Diversified Portfolios generally including more asset classes than more traditional portfolios. Generally the purpose of such presentations is to demonstrate the impact of added diversification.

Although we have done our best to present this information fairly, hypothetical performance is still potentially misleading. Hypothetical data does not represent actual performance and should not be interpreted as an indication of actual performance. This data is based on transactions that were not made. Instead, the trades were simulated, based on knowledge that was available only after the fact and thus with the benefit of hindsight. Results do not include the impact of taxes, if any. Past performance is not indicative of future performance.

General Information

This website content is subject to change without notice and, due to the rapidly changing nature of the security markets, may quickly become outdated. All materials presented are compiled by Patton from sources believed to be reliable and current, but accuracy cannot be guaranteed. This information is distributed for education purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, product, or service. Content is prohibited from being reproduced.

Diversification does not ensure a profit or protect against a loss in a declining market.

Investments involve risk and unless otherwise state, are not guaranteed. Consider the investment objectives, risks, and expenses carefully before investing.

Readers of the information contained on this website should be aware that any action taken by the viewer/reader based on this information is taken at their own risk. This information does not address individual situations and should not be construed or viewed as any type of individual or group recommendation. Be sure to first consult with a qualified financial adviser, tax professional, and/or legal counsel before implementing any securities, investments, or investment strategies discussed.

Exchange-Traded Funds and Index Mutual Funds (“Index Funds”). All Index Funds are subject to risk, which may result in the loss of principal. International Index Funds involve additional risks, including currency fluctuations and political uncertainty. Index Fund products that invest in emerging markets are generally more risky than those that invest in developed countries because countries with emerging markets may have relatively unstable and less-established markets and economies. Sector Index Funds are subject to sector risks and non-diversification risks, which may result in performance fluctuations that are more extreme than fluctuations in the overall stock market. In addition, sector Index Funds that sample their target indexes to comply with tax diversification rules may experience a greater degree of tracking error than other Index Funds. Prices of mid- and small-cap stocks often fluctuate more than those of large-company stocks.

Source Data for Analysis

Any analysis reflecting daily performance for any Patton Investment Strategy is an actual data for the periods available and back-tested data for prior periods. Daily data for diversified portfolios uses an applicable index fund (see the Asset Classes table in this Disclosure "Index Fund" column) performance less the applicable fees.

Mutual fund performance and performance statistics come from Steele Mutual Fund Expert (https://steelesystems.com/).

Client Performance Reporting

Client performance reporting, illustrated as the "Family", in the password protected areas of our webiste, including our Super-Diversified Portfolio Statements section, does represent the actual performance of an individual client's portfolio. Returns are shown net of fees, deposits, and withdrawals. These returns are calculated consistent with industry standards (returns are linked for periods upon a deposit or withdrawal).

Every effort is made to insure correct calculations. Please notify Patton if you believe your returns do not appear correct.

For clients with an investment in a Patton hedge fund / L.P., all current date valuations and daily returns for hedge fund investments are an estimate. These estimates are based on your most recent actual month-end balance, if applicable, and incremented by the estimated daily percent change. Month-end market valuations are actual once the hedge fund statement has been posted to the website.

Performance for specific asset classes does NOT represent the actual performance for the client; this performance is for the asset class based on the assumptions and descriptions made in our Asset Classes Descriptions in our full disclosure.

Any reference to the "Benchmark" portfolio is a simulated portfolio. This does not represent actual returns. It is used as a simulated benchmark to compare to the client's actual performance. See the "Benchmark Portfolio" report in the Dashboard reports for details about the asset allocation and more of the Benchmark Portfolio.

Portfolio Performance Composites

We have multiple portfolio performance composites. Each portfolio performance composite represents a different portfolio strategy and a different risk profile. Generally all Patton client portfolios that meet the minimum value, typically $100,000, are included in one of the portfolio performance composites. Portfolios may be excluded for various reasons and periods of time when it is deemed their performance is not representative of the Composite (example: use of margin). Portfolios are generally added to a Composite for the first full month it is invested and removed after the last full month it is invested. The result is multiple performance composites consisting of all like-type (strategy and risk profile) Patton client portfolios.

Following are the strategies for the portfolio performance composites:

Super-Diversified with Flex: diversified portfolios including an allocation to the Patton Flex Strategy or Patton Flex Fund, L.P.

Super-Diversified with Audacity: diversified portfolios including an allocation to the Audacity Strategy or Audacity Fund, L.P.

Better-Diversified: diversified portfolios without an allocation to any Patton strategy

The three diversified portfolio performance composites are further separated by the following risk profiles: Conservative, Moderate, and Growth.

All references to "Patton Clients" on our website represents the Super-Diversified with Flex performance composite for the Growth risk profile.

Use of leverage on a portion of the portfolios represented by this composite return has had a material impact on the performance figures displayed.

Performance is calculated as a dollar-weighted average meaning that larger accounts have a larger impact on the composite average.

Performance is shown net of client fees.

The following table provides details for each portfolio performance composite:

Portfolio Performance Composite Details

Performance

Date

Composite

Client Count

Client Assets

02/28/2010

-1.02%

1

2,813,735

02/28/2010

0.22%

1

860,504

02/28/2010

1.99%

1

459,585

02/28/2010

2.44%

1

157,368

02/28/2010

2.65%

1

1,278,543

02/28/2010

2.65%

1

1,278,543

02/28/2010

3.00%

2

771,810

02/28/2010

3.76%

2

1,336,988

02/28/2010

5.09%

2

850,555

03/31/2010

2.26%

1

872,901

03/31/2010

3.13%

1

473,941

03/31/2010

3.39%

1

1,321,851

03/31/2010

3.39%

1

1,321,851

03/31/2010

3.60%

2

266,296

03/31/2010

3.79%

2

801,196

03/31/2010

8.31%

2

921,205

03/31/2010

9.05%

1

2,947,202

03/31/2010

9.42%

2

1,398,989

04/30/2010

0.30%

1

1,441,106

04/30/2010

0.30%

1

1,441,106

04/30/2010

0.72%

2

927,576

04/30/2010

1.19%

2

810,995

04/30/2010

1.24%

1

479,910

04/30/2010

1.74%

3

675,594

04/30/2010

2.84%

2

1,412,357

04/30/2010

3.23%

1

888,044

04/30/2010

4.60%

1

3,003,168

05/31/2010

-7.08%

2

851,554

05/31/2010

-5.75%

3

637,248

05/31/2010

-5.70%

2

1,333,337

05/31/2010

-4.51%

2

774,285

05/31/2010

-4.47%

1

458,425

05/31/2010

-3.46%

1

2,899,045

05/31/2010

-0.10%

1

1,440,223

05/31/2010

-0.10%

1

1,440,223

05/31/2010

-0.04%

1

886,585

06/30/2010

-9.21%

2

772,867

06/30/2010

-2.23%

1

2,860,101

06/30/2010

-0.51%

1

1,586,078

06/30/2010

-0.51%

1

1,586,078

06/30/2010

-0.50%

2

770,619

06/30/2010

-0.37%

2

1,327,316

06/30/2010

-0.34%

3

635,852

06/30/2010

1.12%

1

463,588

06/30/2010

4.56%

1

907,154

07/31/2010

0.89%

1

1,600,636

07/31/2010

0.89%

1

1,600,636

07/31/2010

3.20%

1

478,386

07/31/2010

3.72%

2

799,238

07/31/2010

3.75%

1

2,906,405

07/31/2010

3.75%

3

1,887,802

07/31/2010

3.91%

2

1,459,963

07/31/2010

5.11%

3

668,177

07/31/2010

5.79%

2

817,869

08/31/2010

-5.80%

2

745,128

08/31/2010

-4.05%

3

1,844,964

08/31/2010

-2.10%

1

2,871,113

08/31/2010

-1.75%

1

1,169,467

08/31/2010

-1.47%

2

1,466,267

08/31/2010

-1.14%

2

790,146

08/31/2010

-0.86%

3

662,481

08/31/2010

-0.02%

1

478,354

08/31/2010

0.66%

1

1,192,384

08/31/2010

2.23%

1

119,409

09/30/2010

-0.19%

1

1,072,749

09/30/2010

-0.19%

1

1,072,749

09/30/2010

1.98%

1

121,794

09/30/2010

4.38%

2

824,690

09/30/2010

4.50%

1

499,989

09/30/2010

5.76%

3

700,676

09/30/2010

7.43%

2

1,501,957

09/30/2010

9.88%

1

3,012,465

09/30/2010

10.88%

1

214,524

09/30/2010

10.88%

3

1,943,774

10/31/2010

0.23%

1

122,038

10/31/2010

0.87%

1

504,349

10/31/2010

1.10%

1

1,151,313

10/31/2010

1.10%

1

1,151,313

10/31/2010

1.13%

3

708,819

10/31/2010

1.21%

1

3,048,665

10/31/2010

1.28%

2

835,266

10/31/2010

1.66%

2

1,518,380

10/31/2010

2.24%

3

1,987,389

10/31/2010

4.15%

2

851,157

11/30/2010

-1.25%

1

120,530

11/30/2010

-0.95%

3

702,071

11/30/2010

-0.85%

1

1,141,385

11/30/2010

-0.85%

1

1,141,385

11/30/2010

-0.84%

3

1,973,588

11/30/2010

-0.49%

1

500,018

11/30/2010

-0.48%

2

831,439

11/30/2010

-0.34%

2

1,507,515

11/30/2010

0.28%

1

3,000,477

11/30/2010

1.71%

2

865,824

12/31/2010

-0.76%

1

119,624

12/31/2010

0.10%

1

1,142,400

12/31/2010

0.10%

1

1,142,400

12/31/2010

0.99%

2

1,509,912

12/31/2010

1.05%

2

1,523,997

12/31/2010

1.71%

1

4,155,828

12/31/2010

3.08%

1

3,092,127

12/31/2010

3.17%

2

1,509,912

12/31/2010

3.28%

2

858,710

12/31/2010

3.30%

1

424,236

12/31/2010

3.93%

3

729,696

12/31/2010

5.17%

2

890,733

01/31/2011

-0.22%

1

1,130,512

01/31/2011

0.07%

1

4,158,834

01/31/2011

0.13%

1

119,751

01/31/2011

0.25%

2

1,527,259

01/31/2011

0.25%

2

860,903

01/31/2011

0.33%

2

1,514,679

01/31/2011

0.33%

2

1,514,679

01/31/2011

0.39%

3

732,530

01/31/2011

0.60%

1

426,735

01/31/2011

0.83%

1

1,152,024

01/31/2011

1.44%

3

1,092,983

01/31/2011

14.46%

1

3,106,906

02/28/2011

-11.09%

1

3,195,012

02/28/2011

1.17%

1

121,154

02/28/2011

1.45%

1

1,201,195

02/28/2011

1.45%

1

1,201,195

02/28/2011

2.25%

2

1,561,848

02/28/2011

2.57%

1

4,265,778

02/28/2011

2.92%

2

885,913

02/28/2011

2.96%

1

439,430

02/28/2011

3.06%

3

754,862

02/28/2011

3.25%

2

1,563,578

02/28/2011

3.25%

2

1,563,578

02/28/2011

3.49%

3

1,131,021

03/31/2011

-1.44%

1

1,183,906

03/31/2011

-1.44%

1

1,183,906

03/31/2011

-0.08%

1

121,067

03/31/2011

0.02%

1

4,265,396

03/31/2011

0.08%

1

3,147,406

03/31/2011

0.09%

2

1,563,365

03/31/2011

0.32%

3

2,111,465

03/31/2011

0.32%

3

2,111,465

03/31/2011

0.35%

3

757,372

03/31/2011

0.42%

1

441,175

03/31/2011

0.43%

2

950,170

03/31/2011

1.04%

3

1,142,789

04/30/2011

0.17%

1

1,227,265

04/30/2011

0.17%

1

1,227,265

04/30/2011

2.52%

2

974,315

04/30/2011

2.57%

1

4,375,424

04/30/2011

2.63%

1

124,268

04/30/2011

2.68%

2

1,604,862

04/30/2011

2.93%

1

454,146

04/30/2011

2.93%

1

3,240,220

04/30/2011

3.12%

4

940,317

04/30/2011

3.22%

2

1,881,876

04/30/2011

3.22%

2

1,881,876

04/30/2011

3.24%

3

1,149,138

05/31/2011

-1.33%

3

2,149,946

05/31/2011

-1.33%

3

2,149,946

05/31/2011

-1.25%

2

962,025

05/31/2011

-1.16%

1

448,884

05/31/2011

-1.15%

4

929,549

05/31/2011

-0.59%

3

1,142,659

05/31/2011

-0.43%

1

4,356,579

05/31/2011

-0.12%

2

1,602,742

05/31/2011

0.66%

1

1,435,618

05/31/2011

0.66%

1

1,435,618

05/31/2011

0.97%

1

125,494

05/31/2011

3.20%

1

2,721,099

06/30/2011

-2.19%

1

439,013

06/30/2011

-2.15%

4

909,028

06/30/2011

-1.55%

2

424,771

06/30/2011

-1.53%

1

123,567

06/30/2011

-1.43%

1

2,681,971

06/30/2011

-1.41%

2

948,313

06/30/2011

-0.68%

2

1,635,507

06/30/2011

-0.64%

1

4,327,495

06/30/2011

-0.60%

3

2,137,255

06/30/2011

-0.60%

3

2,137,255

06/30/2011

2.73%

1

1,518,794

06/30/2011

2.73%

1

1,518,794

07/31/2011

-2.40%

3

1,088,326

07/31/2011

-1.05%

1

1,502,394

07/31/2011

-1.05%

1

1,502,394

07/31/2011

-0.02%

1

2,622,661

07/31/2011

-0.02%

4

2,755,780

07/31/2011

-0.02%

4

2,755,780

07/31/2011

0.01%

5

1,817,858

07/31/2011

0.23%

2

950,747

07/31/2011

0.24%

1

439,950

07/31/2011

0.48%

1

4,347,839

07/31/2011

0.80%

2

1,704,733

07/31/2011

2.11%

1

126,172

08/31/2011

-6.06%

3

1,022,837

08/31/2011

-3.50%

4

2,660,014

08/31/2011

-3.50%

4

2,660,014

08/31/2011

-2.28%

5

1,776,146

08/31/2011

-2.28%

1

429,884

08/31/2011

-1.48%

2

936,957

08/31/2011

-0.97%

2

1,686,004

08/31/2011

-0.69%

1

2,604,500

08/31/2011

-0.35%

1

4,332,719

08/31/2011

2.06%

1

113,494

08/31/2011

7.32%

1

1,462,787

08/31/2011

7.32%

1

1,462,787

09/30/2011

-10.43%

2

349,054

09/30/2011

-6.18%

5

1,666,129

09/30/2011

-5.30%

1

407,123

09/30/2011

-4.81%

4

2,532,186

09/30/2011

-4.81%

4

2,532,186

09/30/2011

-3.75%

1

4,170,624

09/30/2011

-3.68%

2

902,291

09/30/2011

-1.68%

2

1,656,889

09/30/2011

-0.89%

1

2,581,617

09/30/2011

0.37%

2

216,842

09/30/2011

4.24%

1

1,524,712

09/30/2011

4.24%

1

1,524,712

10/31/2011

-2.09%

1

1,492,902

10/31/2011

-2.09%

1

1,492,902

10/31/2011

2.10%

2

221,371

10/31/2011

3.46%

2

1,713,886

10/31/2011

4.21%

1

4,345,771

10/31/2011

5.23%

1

2,716,516

10/31/2011

5.93%

2

956,000

10/31/2011

5.95%

4

2,682,175

10/31/2011

5.95%

4

2,682,175

10/31/2011

7.95%

1

439,510

10/31/2011

8.10%

5

1,802,230

10/31/2011

11.24%

3

1,008,274

11/30/2011

-2.74%

3

980,773

11/30/2011

-0.52%

1

437,226

11/30/2011

-0.32%

6

1,918,713

11/30/2011

-0.06%

2

221,294

11/30/2011

0.07%

1

4,348,533

11/30/2011

0.34%

2

959,238

11/30/2011

0.58%

1

2,673,541

11/30/2011

0.69%

2

1,725,245

11/30/2011

0.70%

4

2,674,875

11/30/2011

0.70%

4

2,674,875

11/30/2011

10.08%

1

1,615,486

11/30/2011

10.08%

1

1,615,486

12/31/2011

-0.29%

6

1,913,707

12/31/2011

0.02%

3

953,926

12/31/2011

0.26%

1

438,420

12/31/2011

0.56%

1

4,374,241

12/31/2011

0.62%

3

1,068,266

12/31/2011

1.11%

2

223,825

12/31/2011

1.35%

4

2,708,428

12/31/2011

1.35%

4

2,708,428

12/31/2011

1.64%

1

2,717,184

12/31/2011

1.86%

2

1,756,639

12/31/2011

7.71%

1

1,739,954

12/31/2011

7.71%

1

1,739,954

01/31/2012

-6.13%

1

1,866,457

01/31/2012

-6.13%

1

1,866,457

01/31/2012

0.67%

2

1,768,736

01/31/2012

1.45%

5

2,951,565

01/31/2012

1.45%

5

2,951,565

01/31/2012

2.04%

3

973,436

01/31/2012

2.30%

2

228,964

01/31/2012

2.43%

1

2,783,574

01/31/2012

2.65%

3

1,096,684

01/31/2012

2.89%

1

4,500,901

01/31/2012

4.26%

1

457,061

01/31/2012

4.44%

6

1,999,558

02/29/2012

0.10%

2

229,115

02/29/2012

1.61%

1

4,573,802

02/29/2012

1.82%

1

465,483

02/29/2012

1.85%

6

2,037,241

02/29/2012

2.04%

2

1,804,917

02/29/2012

2.31%

4

4,049,105

02/29/2012

3.04%

6

3,197,958

02/29/2012

3.04%

6

3,197,958

02/29/2012

3.72%

3

1,009,813

02/29/2012

4.14%

1

1,943,670

02/29/2012

4.14%

1

1,943,670

02/29/2012

4.82%

1

2,846,108

03/31/2012

-0.92%

2

216,897

03/31/2012

0.11%

1

465,889

03/31/2012

0.42%

6

2,046,131

03/31/2012

1.84%

1

4,658,554

03/31/2012

1.92%

1

2,847,957

03/31/2012

2.23%

4

4,137,954

03/31/2012

2.37%

2

1,949,491

03/31/2012

3.80%

3

1,048,764

03/31/2012

4.48%

6

3,341,436

03/31/2012

4.48%

6

3,341,436

03/31/2012

14.86%

1

2,370,736

03/31/2012

14.86%

1

2,370,736

04/30/2012

0.36%

6

2,054,005

04/30/2012

0.55%

2

387,250

04/30/2012

0.61%

1

468,724

04/30/2012

0.94%

4

4,178,579

04/30/2012

1.67%

2

220,581

04/30/2012

1.95%

2

1,986,877

04/30/2012

1.98%

1

2,904,171

04/30/2012

2.31%

6

3,415,476

04/30/2012

2.31%

6

3,415,476

04/30/2012

9.15%

1

2,587,528

04/30/2012

9.15%

1

2,587,528

05/31/2012

-6.23%

2

363,121

05/31/2012

-4.19%

6

1,968,413

05/31/2012

-4.09%

5

4,738,219

05/31/2012

-4.01%

1

128,923

05/31/2012

-3.42%

5

2,036,338

05/31/2012

-3.42%

5

2,036,338

05/31/2012

-2.30%

1

2,577,967

05/31/2012

-2.30%

1

2,577,967

05/31/2012

-2.08%

2

1,945,535

05/31/2012

-1.89%

1

2,849,703

05/31/2012

0.18%

2

220,981

06/30/2012

0.93%

2

222,997

06/30/2012

1.94%

2

1,982,797

06/30/2012

2.20%

5

4,843,295

06/30/2012

2.32%

1

2,853,233

06/30/2012

2.35%

2

371,643

06/30/2012

2.41%

1

2,822,732

06/30/2012

2.41%

1

2,822,732

06/30/2012

2.78%

6

2,190,046

06/30/2012

2.78%

6

2,190,046

06/30/2012

2.82%

1

132,569

06/30/2012

2.83%

6

2,023,870

07/31/2012

-0.71%

2

369,080

07/31/2012

1.28%

6

2,048,844

07/31/2012

1.64%

2

226,665

07/31/2012

1.74%

1

134,865

07/31/2012

1.86%

5

4,932,352

07/31/2012

2.29%

2

2,026,977

07/31/2012

2.71%

1

2,929,988

07/31/2012

3.43%

6

2,259,687

07/31/2012

3.43%

6

2,259,687

07/31/2012

9.13%

1

3,080,508

07/31/2012

9.13%

1

3,080,508

08/31/2012

-4.48%

1

2,942,061

08/31/2012

-4.48%

1

2,942,061

08/31/2012

-0.14%

6

2,232,543

08/31/2012

-0.14%

6

2,232,543

08/31/2012

0.24%

2

227,250

08/31/2012

0.26%

1

2,937,600

08/31/2012

0.34%

2

2,033,491

08/31/2012

0.60%

5

4,960,964

08/31/2012

1.41%

1

136,724

08/31/2012

1.42%

6

2,078,906

08/31/2012

3.10%

2

380,513

09/30/2012

0.12%

2

227,522

09/30/2012

0.77%

1

137,814

09/30/2012

0.96%

1

2,905,160

09/30/2012

1.12%

2

2,056,171

09/30/2012

1.30%

6

2,105,600

09/30/2012

1.68%

5

5,044,081

09/30/2012

1.96%

6

2,299,843

09/30/2012

1.96%

6

2,299,843

09/30/2012

2.38%

1

3,036,075

09/30/2012

2.38%

1

3,036,075

09/30/2012

3.03%

2

392,047

10/31/2012

-3.11%

1

2,941,381

10/31/2012

-3.11%

1

2,941,381

10/31/2012

-1.50%

6

2,265,752

10/31/2012

-1.50%

6

2,265,752

10/31/2012

-1.15%

1

136,250

10/31/2012

-1.13%

6

2,082,036

10/31/2012

-1.09%

5

4,987,134

10/31/2012

-1.02%

1

2,875,441

10/31/2012

-1.01%

2

2,036,372

10/31/2012

-0.99%

2

388,128

10/31/2012

-0.67%

2

218,031

11/30/2012

0.91%

2

220,050

11/30/2012

1.00%

1

137,569

11/30/2012

1.11%

6

2,105,183

11/30/2012

1.32%

5

5,051,079

11/30/2012

1.35%

1

2,914,493

11/30/2012

1.49%

2

2,066,707

11/30/2012

1.62%

2

394,405

11/30/2012

2.11%

6

2,313,906

11/30/2012

2.11%

6

2,313,906

11/30/2012

4.75%

1

3,081,334

11/30/2012

4.75%

1

3,081,334

12/31/2012

-1.37%

1

3,114,146

12/31/2012

-1.37%

1

3,114,146

12/31/2012

-1.16%

1

2,912,197

12/31/2012

-0.24%

2

219,542

12/31/2012

0.57%

2

2,078,803

12/31/2012

0.64%

7

3,834,232

12/31/2012

0.64%

7

3,834,232

12/31/2012

1.16%

5

5,109,094

12/31/2012

1.27%

1

139,328

12/31/2012

1.48%

6

2,135,176

12/31/2012

1.78%

2

383,204

01/31/2013

0.08%

2

219,733

01/31/2013

2.77%

2

2,136,948

01/31/2013

2.87%

1

143,313

01/31/2013

2.94%

5

1,178,418

01/31/2013

4.00%

5

5,372,991

01/31/2013

5.11%

7

4,028,607

01/31/2013

5.11%

7

4,028,607

01/31/2013

6.33%

2

407,439

01/31/2013

8.17%

1

2,969,046

01/31/2013

10.85%

1

3,450,899

01/31/2013

10.85%

1

3,450,899

02/28/2013

-0.24%

1

3,442,863

02/28/2013

0.32%

1

143,739

02/28/2013

0.53%

5

1,590,833

02/28/2013

0.73%

2

410,430

02/28/2013

0.76%

1

112,167

02/28/2013

1.14%

4

4,827,004

02/28/2013

1.22%

2

2,162,660

02/28/2013

1.81%

7

4,103,577

02/28/2013

1.81%

7

4,103,577

02/28/2013

2.62%

1

3,010,133

02/28/2013

4.89%

1

3,628,429

03/31/2013

0.51%

1

112,770

03/31/2013

1.52%

1

145,919

03/31/2013

1.74%

5

1,618,007

03/31/2013

2.40%

2

2,214,553

03/31/2013

2.84%

4

5,985,124

03/31/2013

3.42%

1

3,109,209

03/31/2013

4.13%

7

4,275,319

03/31/2013

4.13%

7

4,275,319

03/31/2013

4.19%

1

4,220,423

03/31/2013

4.19%

1

4,220,423

03/31/2013

4.58%

2

429,176

04/30/2013

-0.37%

3

1,137,575

04/30/2013

0.63%

1

3,825,850

04/30/2013

0.63%

1

3,825,850

04/30/2013

0.71%

8

5,084,877

04/30/2013

0.71%

8

5,084,877

04/30/2013

1.15%

2

2,239,307

04/30/2013

1.36%

4

6,065,000

04/30/2013

1.53%

1

114,497

04/30/2013

1.83%

6

2,289,092

04/30/2013

2.13%

1

149,035

04/30/2013

2.86%

1

3,139,930

05/31/2013

-2.12%

1

112,067

05/31/2013

-1.75%

1

146,402

05/31/2013

-1.33%

6

2,259,715

05/31/2013

-0.30%

2

2,232,983

05/31/2013

-0.08%

4

6,400,147

05/31/2013

0.63%

1

3,159,772

05/31/2013

0.80%

1

92,341

05/31/2013

1.21%

8

5,146,004

05/31/2013

1.21%

8

5,146,004

05/31/2013

4.06%

3

1,183,764

05/31/2013

5.91%

1

4,052,190

05/31/2013

5.91%

1

4,052,190

06/30/2013

-4.48%

3

1,130,883

06/30/2013

-2.83%

6

2,195,830

06/30/2013

-2.65%

1

295,692

06/30/2013

-2.40%

1

142,911

06/30/2013

-2.33%

1

3,086,130

06/30/2013

-2.28%

4

6,255,454

06/30/2013

-2.11%

1

109,684

06/30/2013

-1.88%

8

5,057,424

06/30/2013

-1.88%

8

5,057,424

06/30/2013

-1.84%

2

2,190,856

06/30/2013

-0.12%

1

4,070,509

06/30/2013

-0.12%

1

4,070,509

07/31/2013

0.74%

1

110,489

07/31/2013

1.40%

1

4,127,074

07/31/2013

1.40%

1

4,127,074

07/31/2013

2.00%

2

2,234,901

07/31/2013

2.75%

4

6,430,127

07/31/2013

2.79%

8

5,247,480

07/31/2013

2.79%

8

5,247,480

07/31/2013

2.95%

1

3,116,473

07/31/2013

3.12%

1

147,348

07/31/2013

3.38%

6

2,269,184

07/31/2013

3.59%

1

306,233

07/31/2013

5.80%

3

1,187,328

08/31/2013

-6.65%

1

3,952,439

08/31/2013

-6.65%

1

3,952,439

08/31/2013

-3.84%

8

5,044,261

08/31/2013

-3.84%

8

5,044,261

08/31/2013

-3.59%

3

1,144,338

08/31/2013

-3.05%

2

2,166,982

08/31/2013

-2.94%

1

3,024,404

08/31/2013

-2.46%

4

6,276,041

08/31/2013

-2.38%

1

298,989

08/31/2013

-2.32%

6

2,217,228

08/31/2013

-2.27%

1

143,991

08/31/2013

-1.35%

1

109,001

08/31/2013

-1.18%

1

147,171

09/30/2013

1.42%

1

149,291

09/30/2013

1.61%

1

110,758

09/30/2013

2.57%

1

147,702

09/30/2013

2.94%

4

6,462,100

09/30/2013

3.20%

6

2,287,679

09/30/2013

3.25%

1

308,728

09/30/2013

3.44%

1

3,128,164

09/30/2013

3.52%

2

2,243,396

09/30/2013

4.31%

8

5,258,712

09/30/2013

4.31%

8

5,258,712

09/30/2013

5.53%

1

4,170,636

09/30/2013

5.86%

3

1,211,051

09/30/2013

11.51%

1

4,176,526

10/31/2013

-0.80%

1

4,239,524

10/31/2013

-0.80%

1

4,239,524

10/31/2013

0.93%

1

150,669

10/31/2013

1.12%

1

111,992

10/31/2013

1.84%

4

6,583,215

10/31/2013

2.10%

2

2,290,904

10/31/2013

2.25%

1

330,023

10/31/2013

2.30%

6

2,339,938

10/31/2013

2.33%

1

151,126

10/31/2013

2.62%

8

5,590,673

10/31/2013

2.62%

8

5,590,673

10/31/2013

3.32%

1

3,173,775

10/31/2013

4.20%

3

1,251,097

11/30/2013

-0.61%

1

111,298

11/30/2013

-0.18%

1

150,845

11/30/2013

-0.05%

6

2,337,596

11/30/2013

0.08%

1

150,817

11/30/2013

0.31%

1

331,094

11/30/2013

0.99%

4

6,645,809

11/30/2013

1.51%

2

2,325,489

11/30/2013

3.02%

2

3,370,408

11/30/2013

3.17%

2

1,050,982

11/30/2013

3.43%

8

5,829,033

11/30/2013

3.43%

8

5,829,033

11/30/2013

15.53%

1

4,857,468

11/30/2013

15.53%

1

4,857,468

12/31/2013

-0.97%

1

110,223

12/31/2013

-0.24%

1

150,466

12/31/2013

0.31%

6

2,344,681

12/31/2013

0.59%

1

151,729

12/31/2013

0.61%

1

333,058

12/31/2013

0.64%

1

1,251,199

12/31/2013

0.89%

4

6,705,317

12/31/2013

1.86%

2

3,433,349

12/31/2013

1.96%

8

5,948,563

12/31/2013

1.96%

8

5,948,563

12/31/2013

2.05%

1

5,074,023

12/31/2013

2.05%

1

5,074,023

12/31/2013

2.58%

3

1,301,377

01/31/2014

-15.87%

1

4,485,357

01/31/2014

-9.04%

1

4,642,895

01/31/2014

-4.47%

8

5,721,319

01/31/2014

-4.47%

8

5,721,319

01/31/2014

-2.37%

2

3,350,772

01/31/2014

-2.30%

3

1,271,550

01/31/2014

-1.63%

4

6,594,185

01/31/2014

-1.55%

1

327,842

01/31/2014

-1.30%

6

2,315,016

01/31/2014

-1.27%

1

1,235,456

01/31/2014

-1.18%

1

149,962

01/31/2014

0.14%

1

150,695

01/31/2014

1.33%

1

111,671

02/28/2014

0.56%

1

113,057

02/28/2014

1.82%

1

153,396

02/28/2014

3.50%

1

155,190

02/28/2014

3.64%

5

1,734,817

02/28/2014

3.89%

1

340,605

02/28/2014

3.93%

4

6,807,985

02/28/2014

4.00%

2

2,377,623

02/28/2014

4.51%

1

106,662

02/28/2014

5.23%

9

6,257,514

02/28/2014

5.23%

9

6,257,514

02/28/2014

5.73%

3

1,344,329

02/28/2014

6.87%

1

5,183,008

03/31/2014

-1.53%

3

1,323,816

03/31/2014

0.12%

1

113,170

03/31/2014

0.24%

1

153,400

03/31/2014

0.47%

5

1,744,499

03/31/2014

0.58%

1

362,774

03/31/2014

0.73%

3

1,205,324

03/31/2014

0.78%

1

107,331

03/31/2014

0.87%

1

156,549

03/31/2014

0.94%

2

2,394,863

03/31/2014

1.05%

9

6,640,859

03/31/2014

1.05%

9

6,640,859

03/31/2014

1.57%

1

6,236,042

03/31/2014

3.66%

1

7,488,924

04/30/2014

-3.73%

1

105,040

04/30/2014

-1.74%

3

1,300,101

04/30/2014

-1.54%

1

7,498,719

04/30/2014

-0.71%

12

12,835,826

04/30/2014

-0.71%

12

12,835,826

04/30/2014

-0.05%

1

154,112

04/30/2014

0.16%

1

158,201

04/30/2014

0.25%

2

2,401,907

04/30/2014

0.58%

1

364,893

04/30/2014

0.62%

3

1,213,137

04/30/2014

0.73%

5

1,764,023

04/30/2014

0.79%

1

114,057

04/30/2014

2.92%

1

7,498,719

05/31/2014

1.35%

1

115,591

05/31/2014

1.36%

1

156,169

05/31/2014

1.48%

5

1,790,649

05/31/2014

1.50%

1

160,593

05/31/2014

1.68%

1

370,945

05/31/2014

2.22%

3

1,240,044

05/31/2014

3.16%

2

2,477,720

05/31/2014

3.23%

12

13,255,183

05/31/2014

3.23%

12

13,255,183

05/31/2014

3.34%

1

108,689

05/31/2014

3.38%

3

1,319,349

05/31/2014

6.34%

1

8,061,013

05/31/2014

8.64%

1

191,446

06/30/2014

-9.00%

1

8,204,976

06/30/2014

-6.61%

1

8,274,374

06/30/2014

-0.98%

2

2,454,157

06/30/2014

-0.74%

12

13,150,894

06/30/2014

-0.74%

12

13,150,894

06/30/2014

0.09%

1

156,320

06/30/2014

0.20%

3

1,242,315

06/30/2014

0.22%

1

115,830

06/30/2014

0.67%

2

3,474,759

06/30/2014

0.94%

1

162,125

06/30/2014

1.17%

5

1,811,879

06/30/2014

1.22%

1

375,455

06/30/2014

3.19%

3

1,361,133

07/31/2014

-2.43%

3

1,316,087

07/31/2014

-1.94%

1

8,622,633

07/31/2014

-1.61%

3

3,341,853

07/31/2014

-1.57%

12

12,948,989

07/31/2014

-1.57%

12

12,948,989

07/31/2014

-1.56%

1

369,701

07/31/2014

-1.50%

1

785,873

07/31/2014

-1.42%

3

1,043,510

07/31/2014

-1.38%

5

1,787,488

07/31/2014

-1.19%

1

160,216

07/31/2014

-1.18%

2

3,433,340

07/31/2014

-0.35%

1

8,622,633

07/31/2014

-0.33%

1

115,452

07/31/2014

25.33%

1

369,701

08/31/2014

1.96%

4

888,665

08/31/2014

2.11%

1

117,904

08/31/2014

2.72%

2

1,962,967

08/31/2014

2.73%

2

630,527

08/31/2014

2.75%

13

14,002,448

08/31/2014

2.75%

13

14,002,448

08/31/2014

2.81%

1

807,974

08/31/2014

3.06%

1

381,070

08/31/2014

3.14%

1

165,238

08/31/2014

3.24%

5

1,844,506

08/31/2014

3.73%

1

107,585

08/31/2014

5.20%

3

1,384,257

09/30/2014

-3.57%

1

159,323

09/30/2014

-3.44%

6

2,211,260

09/30/2014

-3.19%

1

369,031

09/30/2014

-2.35%

3

1,351,937

09/30/2014

-2.30%

2

616,066

09/30/2014

-1.67%

1

794,439

09/30/2014

-1.65%

1

115,960

09/30/2014

-1.56%

2

1,932,082

09/30/2014

-0.97%

16

17,103,909

09/30/2014

-0.97%

16

17,103,909

09/30/2014

-0.75%

2

3,400,344

09/30/2014

3.72%

1

9,298,273

09/30/2014

8.66%

1

9,262,341

10/31/2014

-1.71%

1

9,362,403

10/31/2014

0.91%

3

1,351,092

10/31/2014

1.63%

1

117,850

10/31/2014

1.92%

3

738,776

10/31/2014

2.20%

2

1,974,234

10/31/2014

2.20%

1

811,896

10/31/2014

2.28%

16

17,467,978

10/31/2014

2.28%

16

17,467,978

10/31/2014

2.35%

2

3,481,137

10/31/2014

2.43%

1

10,008,906

10/31/2014

2.46%

1

378,102

10/31/2014

2.47%

6

2,265,609

10/31/2014

2.53%

1

163,334

11/30/2014

0.45%

1

164,039

11/30/2014

1.04%

7

2,792,514

11/30/2014

1.13%

1

119,191

11/30/2014

1.54%

1

383,941

11/30/2014

2.25%

3

755,537

11/30/2014

3.20%

1

837,803

11/30/2014

3.26%

2

2,038,162

11/30/2014

3.87%

18

20,256,425

11/30/2014

3.87%

18

20,256,425

11/30/2014

4.19%

3

1,407,928

11/30/2014

5.31%

1

116,101

11/30/2014

5.80%

1

10,904,211

11/30/2014

11.76%

6

1,372,922

12/31/2014

-0.68%

5

1,217,149

12/31/2014

-0.67%

1

12,030,016

12/31/2014

-0.47%

1

380,014

12/31/2014

-0.45%

3

1,379,171

12/31/2014

-0.43%

3

752,469

12/31/2014

-0.42%

2

2,029,363

12/31/2014

-0.39%

1

834,654

12/31/2014

-0.38%

18

20,150,000

12/31/2014

-0.38%

18

20,150,000

12/31/2014

0.18%

1

164,277

12/31/2014

0.32%

1

119,551

12/31/2014

1.85%

2

3,555,240

12/31/2014

3.06%

1

11,795,198

01/31/2015

-2.57%

6

1,378,303

01/31/2015

-0.98%

18

19,919,699

01/31/2015

-0.98%

18

19,919,699

01/31/2015

-0.75%

3

1,368,783

01/31/2015

-0.70%

2

1,939,405

01/31/2015

-0.25%

1

832,539

01/31/2015

0.11%

3

753,343

01/31/2015

0.31%

1

381,149

01/31/2015

0.75%

2

3,582,302

01/31/2015

0.96%

6

1,719,247

01/31/2015

1.18%

1

12,444,086

01/31/2015

1.58%

1

166,829

01/31/2015

2.88%

1

123,021

02/28/2015

-1.18%

1

121,555

02/28/2015

0.67%

1

167,933

02/28/2015

1.56%

6

2,099,558

02/28/2015

2.06%

1

15,657,291

02/28/2015

2.44%

1

390,363

02/28/2015

2.86%

3

774,912

02/28/2015

3.22%

1

859,343

02/28/2015

3.60%

2

3,711,622

02/28/2015

3.71%

2

2,084,019

02/28/2015

4.63%

18

20,958,438

02/28/2015

4.63%

18

20,958,438

02/28/2015

4.71%

3

1,433,425

02/28/2015

8.16%

1

15,657,291

03/31/2015

-0.68%

5

1,591,335

03/31/2015

-0.55%

3

770,599

03/31/2015

-0.53%

1

388,312

03/31/2015

-0.39%

3

1,428,426

03/31/2015

-0.11%

2

2,080,960

03/31/2015

-0.08%

18

21,051,339

03/31/2015

-0.08%

18

21,051,339

03/31/2015

0.08%

1

860,229

03/31/2015

0.27%

1

121,879

03/31/2015

0.97%

2

3,650,495

03/31/2015

1.44%

1

15,885,435

03/31/2015

3.53%

1

15,669,485

04/30/2015

-20.57%

1

14,352,101

04/30/2015

-6.31%

2

488,405

04/30/2015

-4.51%

18

21,070,106

04/30/2015

-4.51%

18

21,070,106

04/30/2015

-4.28%

2

3,493,831

04/30/2015

-3.33%

3

1,355,738

04/30/2015

-3.18%

1

832,788

04/30/2015

-2.89%